[ad_1]

The outlook for nickel for the rest of the year is bearish as its production continues to exceed demand. There are also fears of weak economic growth besides disappointing Chinese data. A rise in production of Class two nickel, which has a lower nickel content and is used for manufacturing stainless steel, is also contributing to the dim prospects.

According to the International Nickel Study Group (INSG), the nickel market faces the largest demand-supply surplus in a decade as production in Indonesia and the Philippines is high. Indonesia’s output has already grown to 1.58 million tonnes in the previous year, accounting for nearly half the worldwide supply.

Steady downtrend

A slow recovery in Chinese goods demand in the first half of 2023 has dampened global nickel demand, said the Australian Office of the Chief Economist in its Resource and Energy Quarterly for June. “(Nickel) Prices have been been on a steady downward trend since January 2023, falling to the lowest level seen since September 2022 of $20,305 a tonne on June 26, down 34.7 per cent from the year-to-date high of $31,118 seen on January 3 as excess of Class two nickel floods the market,” research agency BMI, a unit of Fitch Solutions, said.

Goldman Sachs forecast that nickel prices could fall sharply due to a surge in Indonesia and Chinese supplies, with a 12-month price target of $16,000 a tonne. On Thursday, nickel 3-month contracts on the London Metal Exchange dropped to $20,170 a tonne

BMI has cut its price forecast for the metal, used in coins, kitchenware, electronics and electric vehicle batteries, to $23,500 for 2023 from its previous projection of $26,500 in view of significant rise in Class two nickel production, “pushing the market into deeper surplus”.

Supply surpluses evident

Shanghai Metals Market (SMM) said spot premiums in the Chinese nickel market continue to decline. High nickel prices suppressed offtake and “nickel prices will move sideways, with downward pressure”.

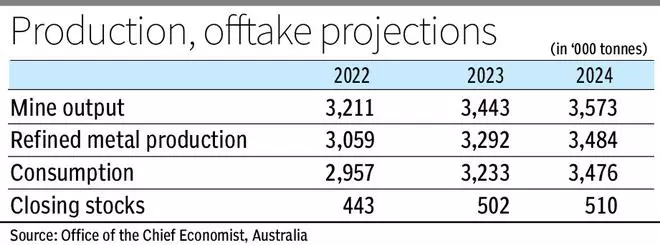

Nickel supply is expected to exceed rising demand, driven by Indonesian (and some Chinese) output growth. Surpluses are evident in Chinese markets, though Western markets remain tight, the Australian Office of Chief Economist said.

ING Think, a unit of Dutch multinational financial services firm ING, said latest data from INSG show that the global nickel market remained in a supply surplus of 20,500 tonnes in April compared with a marginal deficit of 2,600 tonnes in the same period a year ago.

INSG has recently forecast a surplus of 2,39,000 for the global market this year, it said.

Tight inventories

“We expect to see muted gains for the remainder of 2023 as the market remains in surplus, demand continues to be limp and market volatility threatens investor sentiment,” BMI said. However, the research agency said it sees support from tight LME inventories and a weakening US dollar that will prevent prices from collapsing to pre-pandemic levels.

SMM said nickel inventory is still at a historically low level, and the demand has not improved significantly.

ING think said the latest LME data show that warehouses in the US witnessed their first inflows of the metal since September 2021. Total LME stocks in the US are now at 1,506 tonnes, the highest since 2022. Total LME nickel inventories stand at 39,156 tonnes, with the majority of this stored in Asian warehouses.

Indonesia’s output ramp up

BMI said LME inventories are not taking into account the market supply surplus as the surplus is in Class two nickel as it is not traded on the LME.

It said global Class two nickel production will increase significantly in 2023 on the back of a ramp-up in Indonesian and Mainland Chinese refined nickel output, pressuring prices. “We forecast a surplus in the overall nickel market in 2023 of 2,44,700 tonnes, expanding from the surplus of 1,30,600 tonnes seen in 2022,” the research agency said.

The main driver leading to oversupply in the global market is the ramp-up in Indonesia’s output due to greater investment in the country’s downstream nickel industry following the government’s ban on nickel ore exports in January 2020. “In the first three months of 2023, Indonesia’s refined nickel production increased 18.5 per cent year-on-year to 3,02,900 tonnes relative to the 2,55,700 tonnes seen during the same period in 2022,” it said.

Volatility threats

BMI forecast Indonesian nickel production to rise by 20 per cent year-on-year in 2023 with output volumes reaching 5,18,000 tonnes, after a sharp rise in output of 31 per cent year-on-year in 2022.

Supply from Mainland China, world’s largest refined nickel producer, increased sharply with output rising by 27.7 per cent year-on-year to 2,12,000 tonnes in the first three months of 2023.

The research agency forecast Mainland Chinese production to grow by 10 per cent year-on-year to 9,29,000 tonnes in 2023.

On the demand side, nickel prices face additional pressure as global stainless-steel production sees flat growth in 2023, it said.

Low levels of LME nickel stocks continue to pose threats of volatility in the short term, as seen in 2022, BMI said.

The Australian Office of the Chief Economist said a stronger second half in 2023, combined with demand for electric vehicles in the West, is forecast to see nickel usage rise by 9.3 per cent in 2023.

[ad_2]

Source link