[ad_1]

If FY22 was a year of rally in steel prices, FY23 witnessed a similar rally in input costs that impacted the spreads (between realisations and costs). In Q4FY23, steel prices continue to be flattish, but from the inflated base in FY23. The peak commodity costs are most likely behind in FY23 and the medium term will continue to be volatile. We examine the two dynamics and its impact on the bullish capex cycle the companies are currently engaged in.

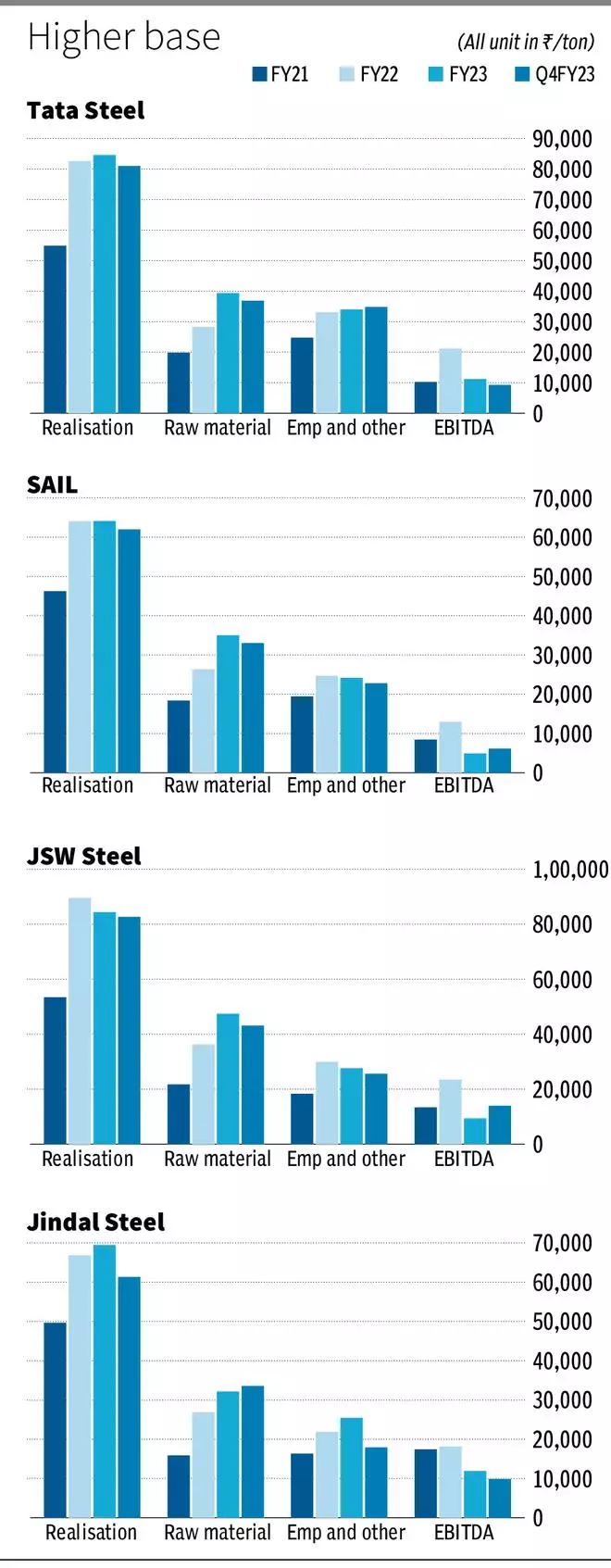

Steel prices hold stead

Steel price realisations across the four leading companies (Tata Steel, SAIL, JSW Steel, and Jindal Steel) gained 35-68 per cent in FY22 as easy monetary policies post-Covid and shortages in production drove realisations. The following year saw a flattish performance ranging from -6 to 4 per cent gain in FY23 as the rally lasted well into the first half of FY23. In the most recent quarter, steel prices corrected but only by an average of 5 per cent across the four compared to FY23 prices, essentially retaining the high base despite modest corrections (see graph). This new base of realisations is 40 per cent higher than FY21.

With expectations of recession in Europe and a slowdown in economic activity in China, factors for strong price growth from the current base cannot be expected. However, offsetting the lack of positive price triggers are supply-side constraints in international steel markets. Europe and even China, accounting for 60-70 per cent of production and demand are facing environmental choke on production. This is either in the form of carbon costs or curtailed manufacturing activity. The higher commodity costs on top of environmental costs are adding downward pressure on industry profitability. The lower utilisation of Russian and Ukrainian steel facility is also adding to price support internationally, despite dampened economic outlook.

Domestically, the removal of export duty and lower Chinese imports is supporting recovery in steel prices to around ₹60,000 per MT (hot rolled coil prices) in April-2023 from a low of ₹55,000 per ton in late CY22. The National Infrastructure Plan will further support prices of core commodities, including steel domestically, along with the current rebound in real estate activity. However, one thing to note is that high interest rates can impact the prospects if inflationary concerns are not addressed.

Also read: Jindal Stainless writes to Finance Ministry seeking duty on Chinese imports

Input cost inflation

Raw material costs per ton doubled between FY21 to Q4FY23 (94 per cent increase), but is gradually declining. Coking coal, which is the primary input cost has come off from $550 per ton last year to $275 per ton currently. Compared to the average for the whole of FY23, the last quarter’s (Q4) RM cost per ton was lower only by an average of 4 per cent across the four companies as the lower costs will be reflected with a lag. EBITDA per ton has improved by 56 per cent QoQ across the four companies gaining from lower raw material costs in Q4FY23. The medium-term outlook though, is hinged on geopolitical outlook and cannot be estimated. The companies have indicated a 4-5 per cent increase in coking coal costs in Q1FY24. But in the long run, the spreads should improve as the decline in realisations is expected to be slower than the decline in raw material costs.

Capex thrust

The Indian companies are on a high capex cycle. Tata Steel is looking to spend ₹16,000 crore in FY24, SAIL ₹6,500 crore, JSW Steel 49,000 crore in three years, and Jindal Steel ₹7,500 crore in FY24. The strong infrastructure push from the government, lower exports from China, restricted supply in Europe, and resulting higher realisations underline the investment plans. Any improvement in input commodities posts geopolitical conflicts should aid the higher capacities with higher spreads. Compared to earlier capex cycles, the companies are at a far better and more comfortable debt position currently with net debt to EBITDA ranging from 0.8 (Jindal Steel) to 3.8 times (SAIL).

With valuations factoring the positives, at bl.portfolio we had recommended investors hold the stock of Tata Steel and recommended buying SAIL ,with its dividend providing comfort

[ad_2]

Source link