[ad_1]

In bl.portfolio’s January15th edition, we carried a primer on chemical industry explaining its transformation over the last decade. As a follow-up, in this article we highlight individual stock’s transformation and valuation re-rating over the last decade. While on a top-down basis, the sector outlook has transformed, all the sector constituents cannot be painted with the same brush.

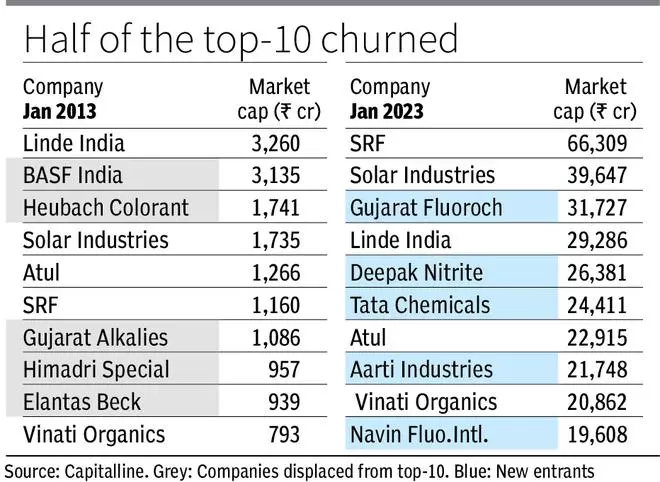

There are quite a few winners and losers in the top 10 companies by market cap from a decade ago. While some stocks have consistently kept pace or outpaced the industry, some others have been relegated to the sidelines and new players have joined the listed space. We look at the most notable changes here.

New entrants and gainers

Prominent amongst the gainers is SRF, which was ranked 6th in January 2013 and moved to its current top spot by January 2018 itself and has retained its leading position since. Similarly, Solar Industries has moved from the 4th spot to its current 2nd spot. Aarti Industries also moved significantly in the period from the 11th spot to the 8th spot now.

However, if the value of its recently demerged Aarti Pharmalabs is also considered, it would actually be in the 3rd spot (this gives a more reflection of its value creation in the last decade). Atul and Vinati Organics have kept pace with industry growth and managed to stay in the top 10, then and now. Linde India, the Indian arm of a German MNC, with 25 per cent market cap CAGR has also managed to retain its leading position.

Gujarat Fluorochemicals, Navin Fluorine, Tata Chemicals, and Deepak Nitrates are the few other companies that have cemented their place in the top 10.

Some of the recently listed companies like Clean Science, Tatva Chintan and Aether Industries while not in the top 10, have raced their way to the top 20 league by value created via their differentiated portfolio.

Moving down the rank

Amongst the industry leaders as on January 2013, BASF India (part of German MNC) even with a decent market cap growth of 15 per cent CAGR in 10 years, has lost its leading position (sector average is at 34 per cent CAGR). Gujarat Alkalies is now ranked 21st according to market cap, compared to its 7th spot 10 years back. Himadri Speciality, which is in the news on account of energy storage solutions, moved down from 8th position in 2013 to 28th position now.

What underlies the churn

Firstly, improved valuations played a part in the sector growth and re-arrangement. The chemicals index (top 10 market cap weighted, rebalanced on a yearly basis) indicates a 34 per cent CAGR growth for the sector in the previous decade compared to 12 per cent CAGR for NIFTY-50 in the same period.

Chemicals industry valuations, based on forward earnings of the two companies with available data, indicate that the PE ratio has moved from 9 and 11 times for SRF and Solar Industries in January 2013 to 28 and 48 times by January 2023 respectively. A CAGR growth of 10-15 per cent in valuations for the two, compared to 5 per cent for NIFTY-50 valuations indicates the extent of re-rating in chemicals stocks. In this process, different companies in the sector got rerated and derated, based on their product portfolio and ability to capitalise on opportunities.

End-user industry, ranging from pharma, agrochem, textiles, FMCG and paints has certainly aided in industry growth. Niche and focussed players like BASF and Gujarat Alkalies have grown slower than the industry, while diversified players (diversified in products, chemistries, and applications) like SRF, Aarti Industries and Atul have done well. Further, Navin Fluorine and Vinati Organics, which have a comparatively narrow product mix but wider application basket have also done well.

[ad_2]

Source link